It

is still very early in the fiscal year so trends in Germany's finances are

relatively meaningless at this point in time. However, there is still

some interesting information to be gleaned from the latest Federal Ministry of Finance Monthly

Report for March 2012 and the March 2012 Federal budget key figures.

Let's

open by looking at a chart showing the fiscal deficit for

January to March of 2011 compared to the same period in 2012 and the projected

deficit for the entire fiscal year:

The

deficit for the three month period was €24.04 billion, down marginally from €25.499

billion one year earlier. Tax revenues were up, however, much of that is

due to special circumstances that will disappear as the year continues. Expenditures

were down, mainly due to reduced spending on social security and interest

payments on the debt. This is not surprising when one considers that interest

rates, courtesy of the Bundesbank and the ECB, are at generational lows.

Total

spending over fiscal 2012 is expected to reach €312.7 billion, up 5.5 percent

from a year earlier with interest expenditures alone estimated to reach 12

percent of total spending at €36.789 billion, up one percentage point from a

year earlier.

Here

is a chart showing Germany's debt stock:

Germany's

debt totals €1.118 trillion ($1.45 trillion US) and consists mainly of Federal

bonds (57 percent of the total debt).

Critically,

as is the case in most of the world's sovereign debt, the majority of Germany's

debt has a fairly short fuse as shown here:

In

the next four years, Germany has €582.6 billion in debt rolling over, 52

percent of their entire outstanding debt. This means that the German

government will be highly susceptible to interest rate fluctuations to the

upside.

Like

most developed nations, the greatest expense to the German government is their

spending on social security-related spending which is estimated to reach €155

billion euros in fiscal 2012, approximately 50.7 percent of all spending. The

next largest expenditure item is for general public services which includes defense;

this will consume €55.2 billion or 18 percent of the budget. Interestingly,

defense spending is expected to reach €31.7 billion or 10.4 percent of total

spending.

Let's

step aside for a moment and look at United States spending on its military compared

to other nations/groups of nations when compared relative to GDP and

population:

In

the first seven months of fiscal 2012, Washington has spent $2.105

trillion; of that, $380 billion or 18 percent of the total was spent on the

military. That is a big difference, isn't it?

Here

is a graph

showing both the inflation-adjusted U.S. military budget and how much of the

world's military spending stems from Washington:

Perhaps

that factor at least partly explains why Germany's fiscal situation looks

relatively pristine when compared to that of the United States!

Germany

anticipates revenues of €279.737 billion over fiscal 2012. This is up a

very marginal €1.2 billion from a year earlier. It would appear that the

German government is not expecting that tax revenues derived from increased

economic growth are going to help balance the budget in 2012.

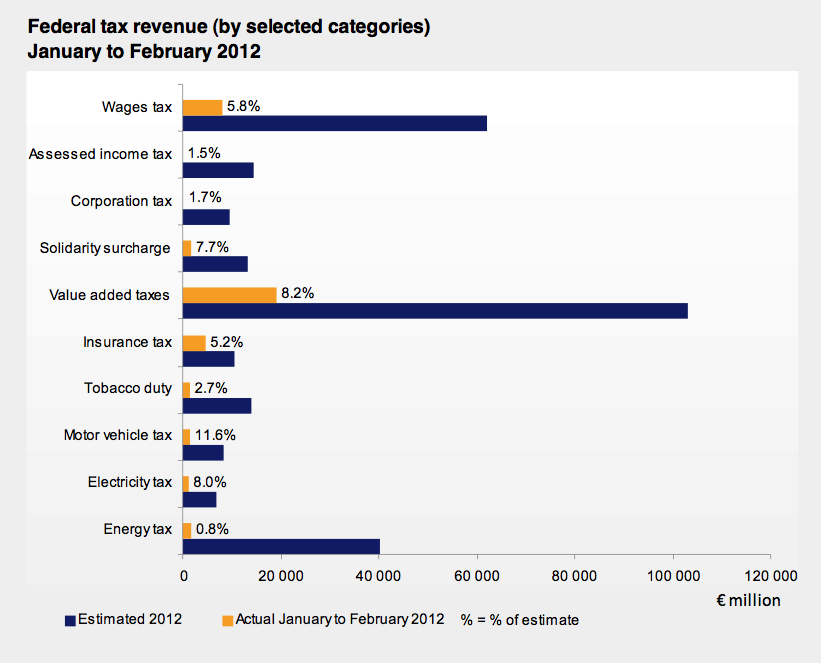

Here

are the sources of revenue for fiscal 2012:

Isn't

it interesting to see that Value Added Taxes (VAT), which has been set at 19 percent since 2007, is expected to be a greater contributor to

overall Federal government revenue than taxes on both wages and energy. VAT

alone is expected to bring in €103.169 billion or 36.9 percent of all revenue

compared to wage taxes which will yield only €62.178 billion or 22.2 percent of

all revenue. I wonder how long it will take Washington to add this little

money-maker to its arsenal of taxation?

In

closing, let's look at a graph that shows how Germany's projected

economic growth looks for fiscal 2012 compared to its fellow Member States:

Eurostat

data projects that Germany's economic growth for 2012 will be a very tepid 0.6

percent. While this is substantially better than its PIIGS counterparts,

it is the same growth rate as the entire EU25 showing that Germany's economy is

not particularly expected to have a spectacular year. As well, Germany's

growth rate of 0.6 percent is well below the growth rates of 3.7 and 3.0

percent that were achieved in 2010 and 2011 respectively. With very

modest economic growth and substantial growth in its debt over fiscal 2012,

Germany's debt-to-GDP ratio is unlikely to fall from 2011's 81.2 percent and,

like the rest of Europe, will likely continue to head skyward.

Over the coming months, particularly as austerity measures

throughout Europe are becoming increasingly unpopular, it will be interesting

to see what happens to Germany's economy and its fiscal situation. With

the economies of the European Community so tightly interlinked, when some

members suffer, even those that appear to be the most prudent will eventually

be dragged into Europe's muck and mire, particularly when in the case of

Germany whose economy relies heavily on exports. Germany's fourth quarter

2011 economic contraction proved that.

You have given awesome information about Federal Ministry of Finance Monthly Report. In this post also very nicely describe Germany's economy and its fiscal situation. So thanks for share this valuable information.

ReplyDelete